Written by Nick Ackerman, co-produced by Stanford Chemist.

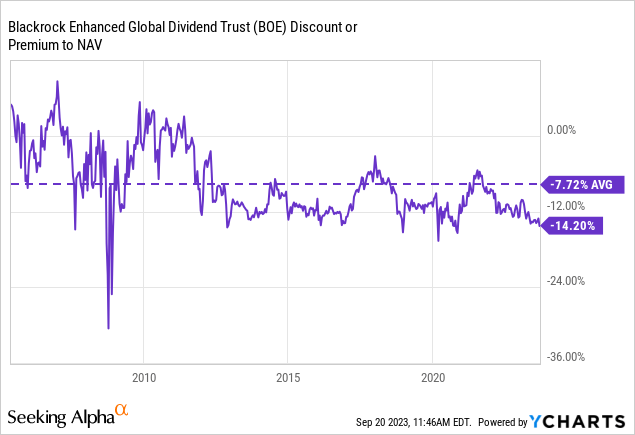

BlackRock Enhanced Global Dividend Trust (NYSE:BOE) continues to see its discount remain wide. While the fund has sported a discount most of the last decade, the latest discount puts it near its widest levels outside of panic selling periods such as Covid.

The fund is weighted towards the tech sector, but it isn’t overly allocated to that area of the market. Additionally, the fund offers global exposure to investors. This approach could provide potential diversification for investors who are looking for more global exposure. On top of this approach, the fund then implements a covered call writing strategy against a portion of the fund’s holdings.

The Basics

1-Year Z-score: -1.50

Discount: -14.20%

Distribution Yield: 7.82%

Expense Ratio: 1.08%

Leverage: N/A

Managed Assets: $705.58 million

Structure: Perpetual

BOE has an investment objective to “provide current income and current gains, with a secondary objective of long-term capital appreciation.”

The fund intends to achieve this through the following:

…investing in at least 80% of its net assets in dividend-paying equity securities and at least 40% of its assets outside of the U.S. The Fund may invest in securities of companies of any market capitalization but intends to invest primarily in securities of large-capitalization companies. The Fund generally intends to write covered put and call options with respect to approximately 30% to 45% of its total assets. However, the percentage may vary from time to time with market conditions.

They focus on writing options on individual stocks in their portfolio. The fund last reported that the portfolio was 44.41% overwritten at the end of July 2023. That is on the higher end of its 30-45% target range. Having more of a portfolio overwritten could suggest that they don’t foresee these positions being called away, which indicates a more defensive stance.

Deep Discount Suggests A Solid Time To Consider The Fund

Since our last update, the fund’s performance has trended upward, but it certainly hasn’t participated to the extent that the tech-heavy S&P 500 has performed. A large part of the returns in what is generally considered the ‘broader market’ has been driven by the mega-cap growth names that have more recently started to be called the Magnificent Seven.

BOE Performance Since Prior Update (BlackRock)

BOE carries a couple of those names, but it generally is more diversified and less exposed to those specific names. As the fund also takes a global approach, that’s one more reason why the S&P 500, in general, isn’t a great benchmark. Then we consider that the fund also takes a covered call approach, and that’s yet another reason.

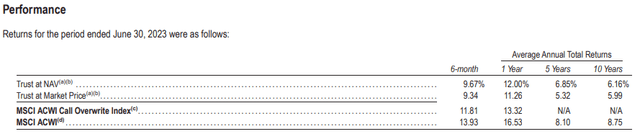

In the fund’s annual and semi-annual reports, they provide better benchmarks that would be more appropriate for comparing performance. The latest semi-annual report just so happened to be posted recently and provides the annualized return performance through the end of June 30, 2023.

When looking at those results, the fund’s historical performance relative to the MSCI ACWI has lagged. However, that index alone doesn’t capture the covered call strategy, which is where the MSCI ACWI Call Overwrite Index comes into play. Unfortunately, in that case, we only have the one-year period to look back on as it’s a relatively newer index. In the one-year period, performance was somewhat comparable, but the fund did lag those results as well.

BOE Annualized Performance (BlackRock)

What an index or ETF can’t offer and is one of the reasons to invest in closed-end funds is to exploit the discount/premium mechanic in the funds. Even if a fund lags marginally in terms of performance, if there is some discount contraction, that can often be enough to produce alpha nonetheless. While BOE has often sported a discount, the current discount provides for an entry near the widest discount levels we’ve seen.

Data by YCharts

Prior to ~2011, this fund had even flirted with a premium on several occasions. That has skewed its longer-term average, but even looking back through most of the period following that, we see that this is pretty much where the fund’s discount has bottomed out. That’s one of the reasons why BOE seems like a fairly compelling option at this time relative to some other global ETFs that may track a global tilted benchmark.

Distribution – Looking Appealing

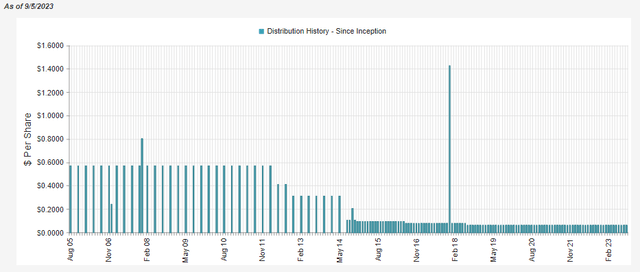

Of course, another reason to invest in a CEF is for more regular distributions from the fund. They often pay managed distributions whereby they attempt to payout-level distributions for years at a time, providing for predictable cash flow. That, of course, doesn’t mean that it is a guaranteed payout, and it can be adjusted from time to time. In the case of BOE, they have had to adjust several times since their inception.

BOE Distribution History (CEFConnect)

They are able to do this and pay out higher distribution rates because they aren’t only paying out income. Instead, they incorporate capital gains and/or return of capital distributions to maintain these higher payouts. The majority of funds are structured as regulated investment companies, which have requirements for paying out almost all of their income and capital gains. So even if they wanted to ‘retain their earnings’ like a C-corp, they would face excise taxes, and then nobody wins except Uncle Sam.

It’s important to note that ROC distributions aren’t always necessarily negative on their own, though this is one of the more confusing topics for newer CEF investors. In fact, there can be some tax-deferral benefits with ROC distributions for investors to take advantage of.

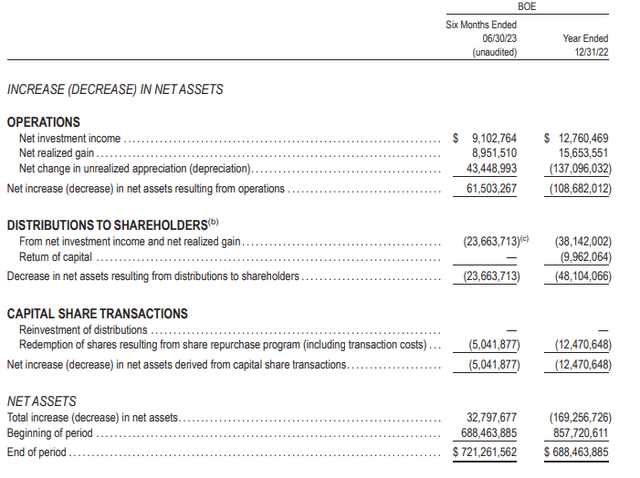

In the first six months of this year, we can see that the fund has pulled in a decent amount of net investor income and realized capital gains. However, they do fall short of covering the distribution to shareholders. At the same time, the unrealized capital gains bucket has also appreciated considerably. As we know, 2022 was a tough year for equities (and fixed-income,) so we are seeing a bit of a recovery from that play out.

BOE Semi-Annual Report (BlackRock)

In a positive trend worth noting, we see that NII has risen quite materially from what they provided for the entirety of 2022. NII can be a more predictable source of coverage because that is the portion that is coming from dividends and interest from underlying holdings. The capital gains, while required in nearly every equity CEF, can be a more unpredictable source, as can naturally be expected.

To highlight the NII in another way, the fund saw NII per share of $0.20 for the entire twelve-month period last year. In this latest six-month period, NII per share has come in at $0.15, equating to an increase of 50% over the prior year if the trend continues in the second half of the year.

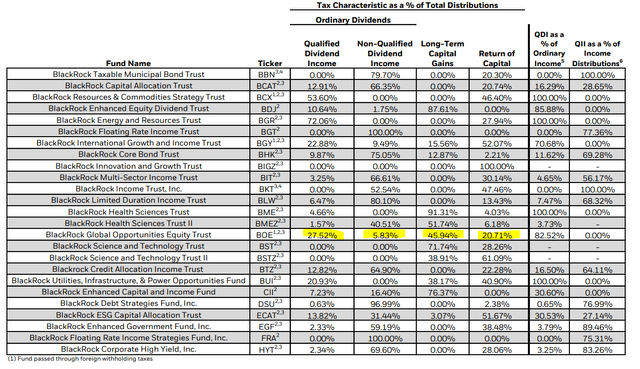

In our prior update, we touched on the distribution tax classifications from the prior year. Here is a quick recap:

For tax purposes in 2022, the fund’s primary classification was long-term capital gains. This was followed by qualified dividends and then return of capital. Given the shortfall in coverage, ROC would have been expected.

BOE Distribution Tax Classification (BlackRock)

The coverage we are seeing in the first half of the year brings up one good example of why there can be some ROC, even if it isn’t technically destructive to the NAV. The fund didn’t realize enough gains in the first half of the year, but the NAV still rose. It could have been that the managers didn’t want to sell off some positions just so they could get a distribution that is classified entirely as capital gains. Instead, they can leave the winners in their portfolio to potentially keep heading higher.

Additionally, this fund had “qualified late-year losses” from 2022. Those are losses that they defer into the next tax year to offset gains. That can also create a situation where even if a fund realizes enough NII and capital gains to fund its distribution, there still can be ROC distributions classified. This is similar to the capital loss carryforwards that some funds are carrying.

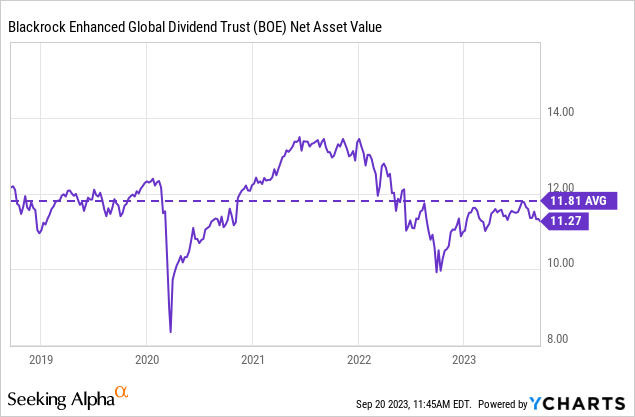

That isn’t to make an excuse for BOE, as the fund has shown considerable NAV erosion historically. They had been overpaying, and that’s why we’ve seen the fund cut its distribution several times. However, the fund has looked much better in the last several years, keeping the NAV fairly flat. I mean, as flat as one would expect to see through the Covid crash and then the 2022 sell-off. It’s an equity fund, after all, that’s going to be volatile, and “flat” is going to be subjective.

Data by YCharts

BOE’s Portfolio

The fund is fairly active, with portfolio turnover coming in at 28% in the first six months of the year. In the last five years, the fund’s average turnover rate has come to 44.8%. However, there aren’t normally too many drastic changes that alter the fund materially.

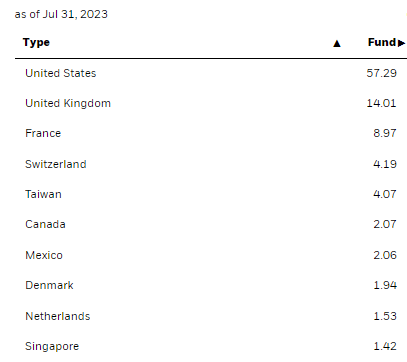

That being said, something worth noting about this latest update is that the fund’s U.S. exposure has actually climbed fairly materially since our last update. Earlier in the year, U.S. exposure was down to around 47.6%. So we’ve seen about a 20.35% increase in the weighting there, which came from reduced exposure across the board to other countries.

BOE Geographic Weighting (BlackRock)

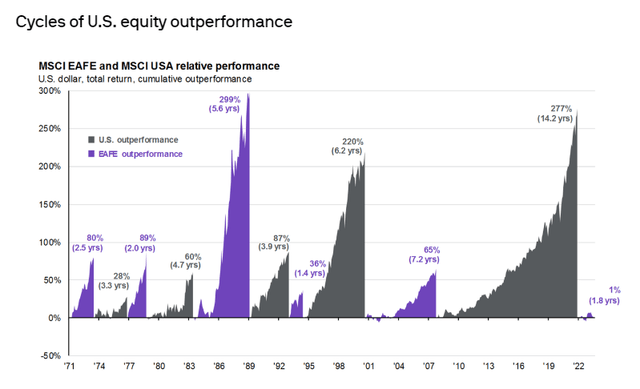

This has happened despite international markets starting to show some glimmers of hope in outperforming more recently. Most investors probably feel like the U.S. is always the place to invest as they’ve “always outperformed.” However, that isn’t exactly the case, as we can see in the chart below.

U.S. Vs. International Equity Performance (JPMorgan)

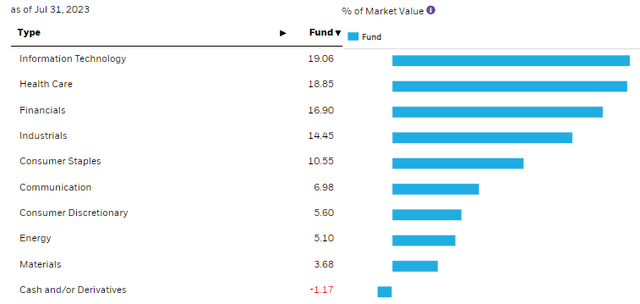

It should also be noted that the fund previously had its largest weighting to the financial and healthcare sectors, and not tech. However, this has since flipped as tech is now the largest sector exposure for the fund. It isn’t an overly large weighting, and it represents a fairly balanced approach to sector allocation, which I find appealing.

BOE Sector Weightings (BlackRock)

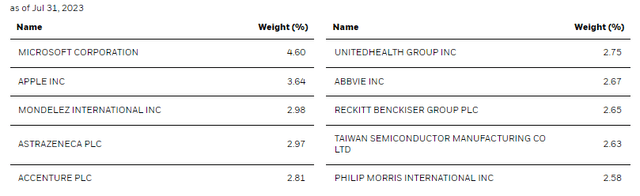

One of the reasons for the shift in U.S. weighting and tech weighting seems to be explained by a new holding in the top ten. Apple (AAPL) is now included as the second largest position in the fund. Also, Microsoft (MSFT) has seen its weighting rise materially from 3.16% to a heavier 4.60%.

BOE Top Ten Holdings (BlackRock)

AAPL shows up as a position in the March 2023 N-PORT, where they list holding 109,789 shares with a weighting of 2.52% of the fund. For Microsoft, we see that they held 109,620 shares with a weight of 4.40%.

At the end of June 2023, AAPL represented 3.65% of the fund – similar to where it is now – with a share balance of 135,913. For MSFT, the weighting had actually risen to 4.74% of the fund, meaning we’ve seen that come down a touch. At that time, they listed holding 100,503 shares.

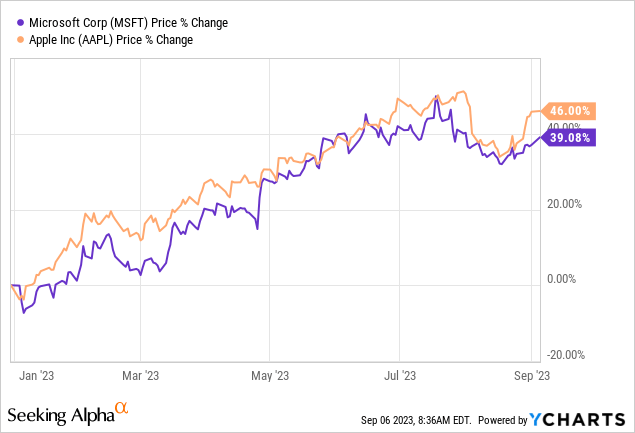

The two changes of seeing increased allocations to AAPL and MSFT can help explain why we’ve seen their portfolio shift. Both of these names are part of the Magnificent 7 stocks. And it’s no surprise both of these names are up massively on a YTD basis – hence why we are seeing the S&P 500 Index itself rise so materially this year.

YCharts

AAPL and MSFT make up 13.88% of the SPDR S&P 500 ETF (SPY), the largest tracking ETF of the S&P 500 Index. So, as we’ve seen the weighting of MSFT rise for BOE, one of the reasons for that is this sort of appreciation in the underlying share price.

Conclusion

BOE continues to trade at an attractive discount. The fund has seen some recovery from the 2022 bear market, though it has some more work to do on that front if it were to get back to 2021 levels. I’m not necessarily hopeful that it would get to that level, but some discount contraction and returns via the distribution would be anticipated to provide some upside potential.

The fund has also seen itself shift toward a heavier allocation to U.S. equities and saw the sector weighting to tech grow to its largest weighting as well. That seems to be explained by adding AAPL to their portfolio through this year. We also saw a significant appreciation in MSFT. While the fund even reduced its position a bit, it has still grown into a larger weighting for the fund. At the same time, I don’t see the sector weightings in this fund as grossly overweight in any specific direction, which is one of the more appealing aspects of the fund, in my opinion.